Your Net Worth: A Clear Path To Financial Understanding

Thinking about your money can feel like a big puzzle, but figuring out your net worth is, in a way, like drawing a clear picture of your financial standing right now. It’s a simple idea, really: what you own minus what you owe. For many people, it helps to see this number grow, or at least understand where it stands. This simple calculation gives you a snapshot, a moment in time, showing you just how much financial ground you have beneath your feet. It’s not about judging your worth as a person; it’s just a tool, a very helpful one, for planning your money journey.

So, why bother with this number? Well, it can show you if you're moving closer to your financial goals, or perhaps if you need to adjust your path a little. It’s a bit like a financial report card, letting you know how you're doing. It’s a personal metric, something just for you, that helps you make smart choices about your spending and saving. It’s about being in the know, you know, about your own money.

This idea of net worth is something anyone can use, whether you're just starting out or have been managing money for years. It helps you see the bigger picture beyond just your monthly paycheck or bills. It's about building something solid over time. It can be a very empowering thing to see your financial health laid out clearly.

- Billy On The Young And The Restless

- Jennifer Lopez In Selena

- Bella Hadid Images

- Garth Brooks Images

- Chatsworth Park North

Table of Contents

- What is Net Worth?

- Why Your Net Worth Matters

- How to Figure Out Your Net Worth

- Including Real Estate in Your Calculations

- Ways to Boost Your Net Worth

- Common Questions About Net Worth

- Keeping Track of Your Net Worth

- Your Financial Journey Ahead

What is Net Worth?

At its core, net worth is a simple math problem: take everything you own, then subtract everything you owe. The number you get is your net worth. It can be positive, which is generally what you want, meaning you own more than you owe. It can also be negative, meaning your debts are more than what your assets are worth. That's just a starting point, not a judgment.

This number changes over time, too. It’s not fixed. As you earn, save, spend, and pay down debt, your net worth moves up or down. It’s a living number, you know, that reflects your financial choices and circumstances. So, tracking it regularly can show you trends, which is pretty useful.

Assets: What You Own

Assets are all the things that have value and belong to you. These are the positive numbers in your net worth calculation. They come in many forms, and understanding them is a big part of getting your financial picture clear. For example, your checking account balance is an asset, and so is your savings account. These are very liquid assets, meaning you can get to that cash easily.

- Tank Singer Movies

- Team Usa Leotards

- Andrew Tate Jake Paul

- December 12th 2024

- Is Ryan Reynolds Christian

Investments are also assets. This includes things like stocks, bonds, mutual funds, and retirement accounts such as 401(k)s or IRAs. These usually grow over time, which is a nice way to build wealth. They are a bit less liquid than cash, but still pretty accessible, generally speaking.

Then there are bigger assets, like your home. As mentioned in my own notes, "In addition to basic accounts, I also would like to include the value of real estate holdings in net worth calculations." This is a very common and important part of many people's net worth. The value of your house, or any other property you own, counts as an asset. This can be a substantial part of your overall financial picture, so it’s something to keep in mind.

Other assets might include vehicles, like cars or motorcycles, if they have significant resale value. Personal belongings, such as valuable jewelry, art, or collectibles, could also be considered assets, though sometimes it's hard to put an exact number on them. For what it's worth, some people include these, others don't, depending on how detailed they want to be. It’s your choice, really, how granular you get with these things.

Liabilities: What You Owe

Liabilities are your debts, the money you still need to pay back. These are the negative numbers in your net worth equation. They can sometimes feel heavy, but they are just a part of financial life for many people. Mortgages, for instance, are a very common liability. This is the money you owe on your home. It’s a big one for most homeowners.

Student loans are another common liability, especially for younger people. These can be quite large and take many years to pay off. Car loans also count here; it’s the money you still owe on your vehicle. These are typically paid off over a few years, so they are a bit more short-term than a mortgage, in a way.

Credit card balances are also liabilities. These can sometimes accumulate quickly if you're not careful. They often carry higher interest rates, so paying these down can be a very smart move for your net worth. Any other personal loans, medical bills, or money you owe to anyone else would also be included here. It’s basically any financial obligation you have, anything that takes money out of your pocket in the future.

Why Your Net Worth Matters

Knowing your net worth is more than just a number; it’s a powerful tool for financial planning. It helps you see where you stand, truly, and gives you a clear picture of your financial health. This can be really helpful for setting goals. For example, if you want to retire by a certain age, knowing your current net worth helps you figure out how much more you need to save and invest. It’s a starting point, basically, for where you want to go.

It also helps you track your progress over time. Seeing your net worth increase can be incredibly motivating. It shows that your efforts to save, invest, and pay down debt are working. Conversely, if it goes down, it can be a signal to look at your spending or income and make some adjustments. It’s a very practical way to measure your financial journey.

Beyond personal goals, your net worth can be important for things like applying for loans or mortgages. Lenders often look at your overall financial picture, and your net worth gives them a quick summary of your assets versus your debts. It shows your financial stability, in some respects. So, it has real-world applications beyond just your own tracking.

How to Figure Out Your Net Worth

Calculating your net worth is quite straightforward, honestly. You just need two lists: one for everything you own (your assets) and one for everything you owe (your liabilities). Start by gathering all your financial statements. This means bank statements, investment account summaries, mortgage statements, loan statements, and credit card bills. Having these in front of you makes the process much easier.

First, list all your assets. Write down the current value of your checking and savings accounts. Add the current market value of your investments, like stocks, bonds, and retirement accounts. Then, list the estimated market value of any real estate you own. For what it's worth, you might use a recent appraisal or online estimates for this. Don't forget any other significant assets, like vehicles or valuable personal items. Add all these numbers together to get your total assets.

Next, list all your liabilities. Write down the outstanding balance on your mortgage, if you have one. Include the total amounts owed on student loans, car loans, and any personal loans. List the current balances on all your credit cards. Add up all these numbers to get your total liabilities. This part can sometimes feel a bit heavy, but it's important to be accurate.

Finally, subtract your total liabilities from your total assets. The number you get is your net worth. It’s that simple. Doing this regularly, say once a year or even every six months, can really help you stay on top of your financial picture. It provides a very clear snapshot of your financial health at that moment.

Including Real Estate in Your Calculations

As I mentioned, "In addition to basic accounts, I also would like to include the value of real estate holdings in net worth calculations." This is a very common and often significant part of many people's net worth. Your home, or any other property you own, represents a substantial asset. Its value can fluctuate, but it's generally a long-term investment that can build wealth over time. So, it makes a lot of sense to include it.

When you include real estate, you're looking at its current market value. This isn't what you paid for it, but what it could sell for today. You can get an estimate from online tools, or even better, from a local real estate agent or an appraisal. Then, you subtract any mortgage or loans still owed on that property. The difference is the equity you have in the property, which is the part that contributes to your net worth. It’s pretty important to get this right.

For example, if your home is worth $400,000 and you still owe $200,000 on the mortgage, you have $200,000 in home equity. That $200,000 is an asset that contributes to your net worth. So, it's not just the basic accounts that matter, but these larger holdings too. This gives a much more complete picture of your financial standing, which is really what you're aiming for.

Ways to Boost Your Net Worth

Once you know your net worth, you might want to see it grow. There are two main ways to do this: increase your assets or decrease your liabilities. Often, doing both at the same time can have the biggest impact. It’s like a two-pronged approach, basically, to getting ahead financially. Little steps can make a big difference over time, too.

Grow Your Assets

Increasing your assets means finding ways to accumulate more valuable things. One common way is to save more money. Putting more cash into your savings accounts or high-yield savings accounts means you have more liquid assets. This is a very straightforward way to add to your net worth. It’s about building up that cash cushion, you know?

Investing is another powerful way to grow assets. Putting money into stocks, bonds, or mutual funds can help your money grow over time, thanks to compound interest. Retirement accounts, like a 401(k) or IRA, are especially good for this because they offer tax advantages. Regularly contributing to these accounts can really add up. For what it's worth, starting early with investing can make a huge difference, apparently.

You can also increase assets by earning more money. This might mean getting a raise, taking on a side gig, or starting a small business. The extra income can then be saved or invested, which directly boosts your assets. It’s about finding ways to bring more money in, so you have more to work with. It's really about being proactive with your income.

Reduce Your Liabilities

Reducing your liabilities means paying down your debts. This is often the quickest way to see your net worth improve, especially if you have high-interest debts. Focusing on paying off credit card balances first is often a very smart move. The interest rates on credit cards can be quite high, so getting rid of that debt frees up more of your money for other things. It's like getting a raise, in a way, when you stop paying so much interest.

Accelerating payments on other loans, like student loans or car loans, can also help. Even paying a little extra each month can reduce the total interest you pay and help you become debt-free faster. This frees up cash flow and reduces your financial obligations, which directly increases your net worth. It’s about chipping away at those debts, you know, bit by bit.

Refinancing high-interest debt to a lower interest rate can also be a good strategy. This can make your monthly payments more manageable and help you pay off the principal faster. It’s about being smart with your debt, not just avoiding it. So, looking for better terms on your loans can really help your overall financial health.

Common Questions About Net Worth

People often have similar questions when they start thinking about net worth. It’s a concept that can seem simple but has many nuances. Here are a few common ones, that people often ask, to help clear things up.

What does net worth not include?

Net worth generally doesn't include things that are hard to put a definite monetary value on, or things that aren't easily converted to cash. For instance, your future income from your job is not part of your current net worth. While it's important for your financial future, it's not an asset you own right now. Similarly, things like your education, skills, or personal relationships, while incredibly valuable, are not typically included in a net worth calculation. It’s focused on tangible financial items, usually.

Is net worth the same as income?

No, net worth and income are very different. Income is the money you earn, like your salary, wages, or business profits. It's a flow of money over a period of time, like a month or a year. Net worth, on the other hand, is a snapshot of your financial position at a specific point in time. It's a measure of accumulated wealth, not how much you're earning. You can have a high income but a low net worth if you spend all your money, or a low income but a high net worth if you've saved and invested wisely over many years. They are related, but not the same, apparently.

What is a good net worth by age?

There isn't one single "good" net worth by age, as it really depends on many factors like your career, location, and financial goals. However, there are general benchmarks or averages that some people look at. For example, some financial experts suggest aiming for a net worth equal to your annual salary by age 30, or perhaps three times your salary by age 40. These are just guidelines, though, not strict rules. What matters most is that your net worth is moving in the direction you want it to, and that you're making progress towards your own financial goals. It's very personal, this number.

Keeping Track of Your Net Worth

Regularly checking your net worth is a habit that can truly empower your financial decisions. It doesn't need to be an everyday task, but setting a schedule, like once a quarter or twice a year, can be very beneficial. This consistent check-in helps you see trends and adjust your financial plans as needed. It’s like taking your financial pulse, you know, to see how things are going.

There are many tools available to help you track this. Simple spreadsheets work well for many people, allowing you to manually enter your assets and liabilities. There are also various financial apps and software programs that can link to your accounts and automatically calculate your net worth. These can make the process much quicker and give you real-time updates. It’s pretty convenient, actually, how much technology can help with this.

The key is consistency. By keeping tabs on your net worth, you gain a clearer picture of your financial progress and can make informed choices about saving, spending, and investing. It helps you stay accountable to your own financial goals. For what it's worth, seeing that number grow can be a really motivating thing, apparently, for many people.

Your Financial Journey Ahead

Understanding your net worth is a foundational step on your financial path. It’s not just a number; it’s a reflection of your past choices and a guide for your future decisions. By regularly calculating what you own versus what you owe, you gain clarity and control over your money. This knowledge empowers you to set realistic goals and work towards them with purpose. It’s a very personal metric, but it can be a powerful one.

Think of it as a personal financial report card, giving you insights into where you stand. Whether you're just starting to build your wealth or are well on your way, this simple calculation can help you stay on track. It’s about being informed and making smart moves for your financial well-being. To learn more about managing your money, you might find helpful information on financial planning at a reputable source, for instance, a site like Investopedia.

Keep in mind that your net worth is a dynamic figure. It will change as your life circumstances change, as markets shift, and as you make new financial choices. The important thing is to keep an eye on it and use it as a tool for growth. You can also learn more about financial growth strategies on our site, and perhaps link to this page for more money management tips. It’s all about taking those steps, one after another, towards a stronger financial future.

- What Does A Nanny Do

- Jeff Bridges Hair

- Drowning Lyrics Chris Young

- Allergy D

- Brittney Griner Talking

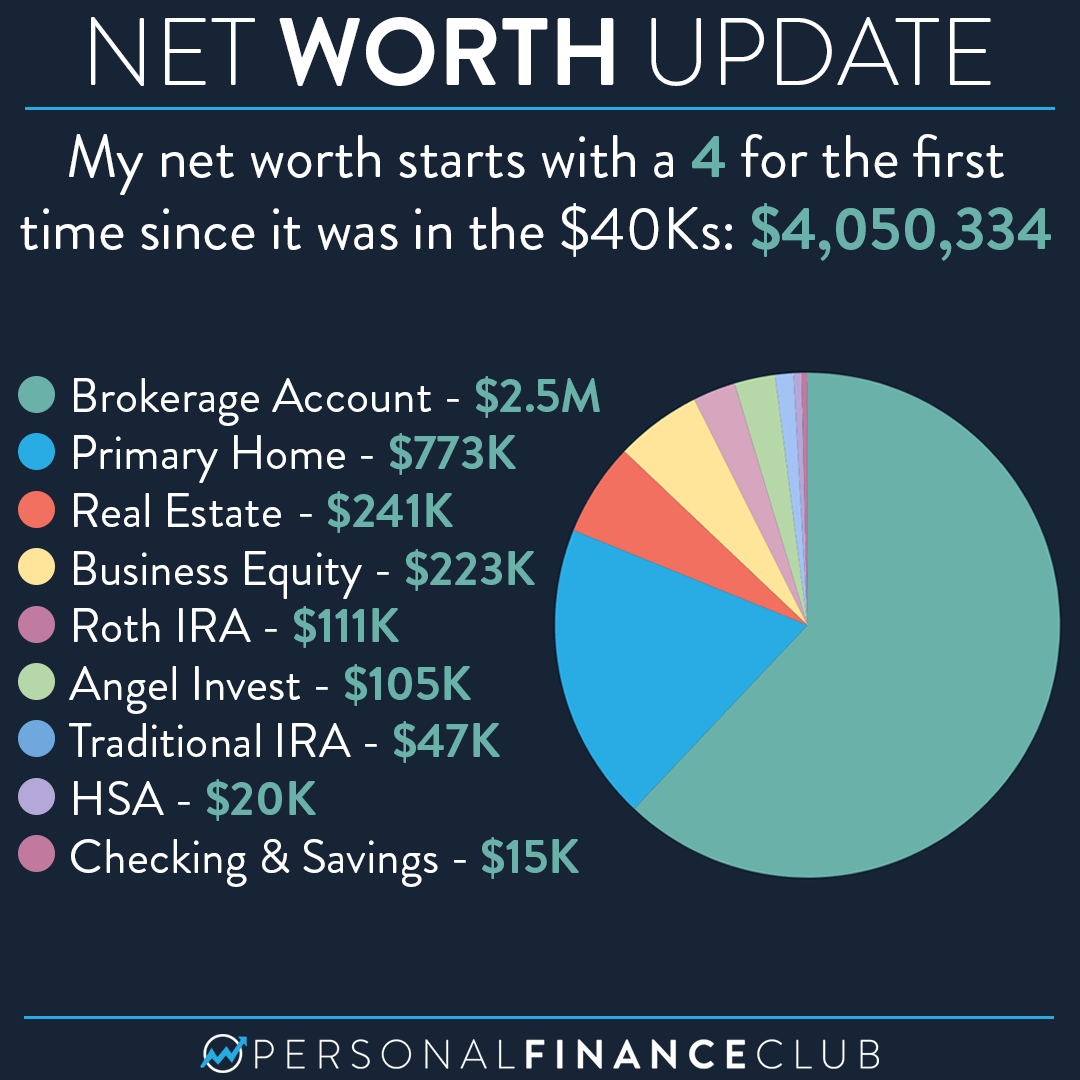

My $4 million net worth breakdown! – Personal Finance Club

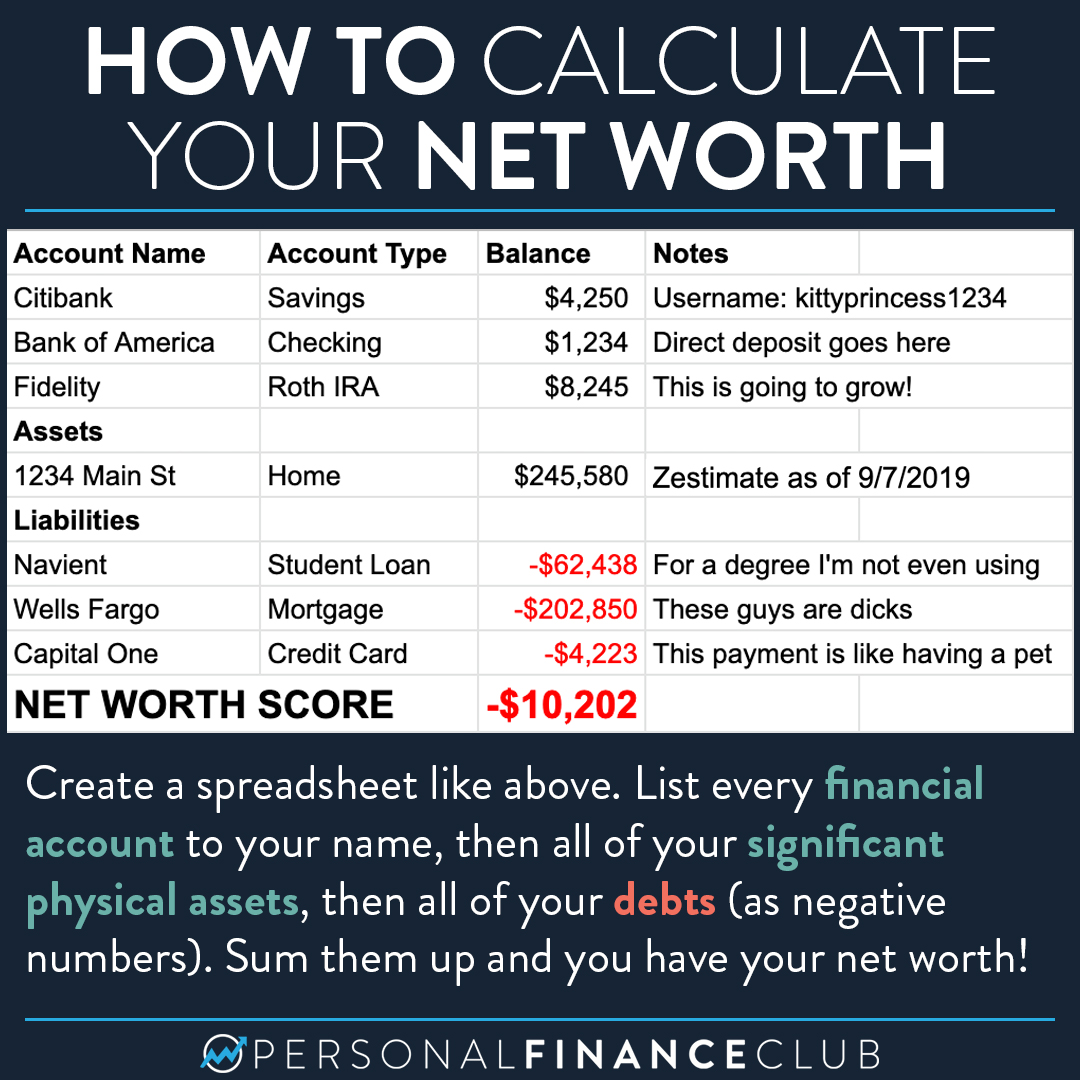

How to calculate your net worth – Personal Finance Club

NET WORTH OF A LIFE